Muni Disclosure: All Talk and No Trade?

Abstract

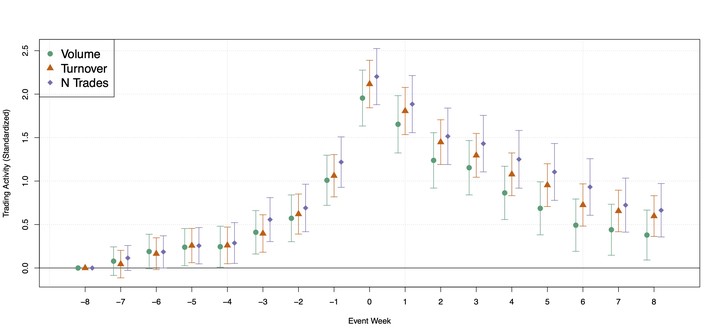

This paper examines which municipal disclosures provide informational value to investors. Using the entire universe of post-issuance financial and event disclosures from 2009 to 2022, we find that most municipal bonds do not trade in the weeks following a disclosure. However, some disclosures do provide enough new information to increase trading. Investors trade more on credit-relevant disclosures, such as adverse credit event disclosures, and less on required annual financial statements. Trading after disclosures also increases more when a bond is large or risky. Moreover, we find that credit rating agencies do respond to disclosures, lending support to the idea that some disclosures have informational value. In further analyses, we find that trading before the disclosure, lack of timeliness, illiquidity, and information processing constraints contribute to the limited trading on the average disclosure. The findings suggest that reconsidering a one-size-fits-all approach to regulating post-issuance municipal disclosures may be worthwhile.

Edward M. Watts

Assistant Professor of Accounting

Edward Watts is an Assistant Professor of Accounting at the Yale School of Management.