Edward Watts

Edward Watts

Home

Publications

Working Papers

Non-refereed Publications

Contact

Publications

Type

Journal article

Report

Date

2026

2025

2024

2023

2022

2021

2020

2018

Information Flows in Trading Networks

We study the informational value of trading networks in over-the-counter (OTC) markets. Using detailed transaction-level data from the …

Stefan Huber

,

Edward M. Watts

,

Christina Zhu

Journal Article

SSRN

CHRO Compensation and Strategic Human Capital Management

Human capital is increasingly the key determinant of productivity; yet, we have a limited understanding of how it is managed within …

David F. Larcker

,

Charles McClure

,

Shawn X. Shi

,

Edward M. Watts

SSRN

The Limited Corporate Response to DEI Controversies

Firms' diversity, equity, and inclusion (DEI) policies have received significant scrutiny in recent years, including their efficacy and …

David F. Larcker

,

Charles McClure

,

Shawn X. Shi

,

Edward M. Watts

SSRN

Muni Disclosure: All Talk and No Trade?

This paper examines which municipal disclosures provide informational value to investors. Using the entire universe of post-issuance …

Christine Cuny

,

Ken Li

,

Anya Nakhmurina

,

Edward M. Watts

Journal Article

SSRN

Information Acquisition Costs and Price Informativeness: Global Evidence

We study how global changes in information acquisition costs through disclosure technologies affect price informativeness. To provide …

Charles McClure

,

Shawn Shi

,

Edward M. Watts

Journal Article

SSRN

Diversity Washing

We provide large-sample evidence on whether U.S. publicly traded corporations use voluntary disclosures about their commitments to …

Andrew Baker

,

David F. Larcker

,

Charles McClure

,

Durgesh Saraph

,

Edward M. Watts

Journal Article

SSRN

Retail Investors and ESG News

An important debate exists around the extent to which retail investors make sustainable investments and, if they do, why. We contribute …

Qianqian Li

,

Edward M. Watts

,

Christina Zhu

Journal Article

SSRN

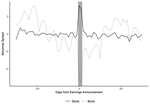

Earnings News and Over-the-Counter Markets

We document significant increases in bond market liquidity around earnings announcements. These increases are attributed to decreased …

Stefan Huber

,

Chongho Kim

,

Edward M. Watts

Journal Article

SSRN

Board Diversity and Shareholder Voting

The lack of diversity across gender and race of corporate boards has been one of the most significant issues in corporate board …

Ian Gow

,

David F. Larcker

,

Edward M. Watts

Journal Article

SSRN

Retail Bond Investors and Credit Ratings

Using comprehensive data on U.S. corporate bond trades since 2002, we find evidence that retail bond investors overrely on untimely …

Ed deHaan

,

Jiacui Li

,

Edward M. Watts

Journal Article

SSRN

ESG Ratings: A Compass Without Direction

David F. Larcker

,

Lukasz Pomorski

,

Brian Tayan

,

Edward M. Watts

Article

SSRN

Firing and Hiring the CEO: What Does CEO Turnover Data Tell Us About Succession Planning?

David F. Larcker

,

Brian Tayan

,

Edward M. Watts

Article

SSRN

Seven Myths of ESG

Environmental, social and governance (ESG) considerations have dominated the discussion of corporate purpose in recent years. We …

David F. Larcker

,

Brian Tayan

,

Edward M. Watts

Journal Article

SSRN

Stock-Option Financing in Pre-IPO Companies

David F. Larcker

,

Brian Tayan

,

Edward M. Watts

Article

SSRN

Tick Size Tolls: Can a Trading Slowdown Improve Earnings News Discovery?

This study examines how an increase in tick size affects algorithmic trading (AT), fundamental information acquisition (FIA), and the …

Charles M.C. Lee

,

Edward M. Watts

Journal Article

SSRN

Sharing the Pain: How Did Boards Adjust CEO Pay in Response to COVID-19?

Amit Batish

,

Andrew Gordon

,

David F. Larcker

,

Brian Tayan

,

Edward M. Watts

,

Courtney Yu

Article

SSRN

From Implicit to Explicit: The Impact of Disclosure Requirements on Hidden Transaction Costs

This paper provides evidence that disclosing corporate bond investors' transaction costs (markups) affects the size of the markups. …

Christine Cuny

,

Omri Even-Tov

,

Edward M. Watts

Journal Article

SSRN

Where's the Greenium?

In this study, we investigate whether investors are willing to trade off wealth for societal benefits. We take advantage of unique …

David F. Larcker

,

Edward M. Watts

Journal Article

SSRN

Cashing It In: Private-Company Exchanges and Employee Stock Sales Prior to IPO

David F. Larcker

,

Brian Tayan

,

Edward M. Watts

Article

SSRN

Cite

×